Cash flow is how you ensure you have enough cash on hand to cover your basic short-term expenses such as operations and payroll.

Simply put, cash flow describes how money comes into your business and leaves it.

Keep reading to learn how to put together a cash flow statement and how to interpret it so you better understand your company’s financial health.

What a Cash Flow Statement Tells You

A cash flow statement, also known as a statement of cash flows, is a financial statement that tells you how cash and cash equivalents entered into your business and how you spent them over a period of time.

Cash equivalents are assets you can quickly convert into cash (usually within three months), such as treasury bills, money market funds, and certificates of deposit.

By looking at a cash flow statement, you can see your top sources of cash (inflow) and top spending categories (outflow).

How You Can Use a Cash Flow Statement

A cash flow statement can serve several purposes based on who’s looking at it. In general, it gives you an outline of how well you manage your cash by showing how money ebbs and flows through your business.

A cash flow statement can help you understand the top categories bringing in cash to your business and those that are pulling cash out.

By looking at your cash flow statement, you can decide if you need to create more sources of cash or address the outflows costing your business the most.

If you’re selling your business, potential investors use cash flow to see how your business generates and uses money. A potential investor may request several cash flow statements to analyze your company’s financial position over time.

Creditors are another set of people that look at the cash flow statement. When you apply for a loan, the bank looks at your cash flow statement to see whether you can cover your expenses and pay down debt.

How Cash Flow Statements Are Structured

A cash flow statement is organized into three categories representing the three types of cash flow:

- Cash from operating activities

- Cash from investing activities

- Cash from financing activities

The statement also includes total cash and cash equivalents at the beginning and end of the reporting peri

If you have more money at the end of the reporting period than at the beginning, your cash flow is positive. And if you end the period with less cash and cash equivalents than you started, that’s a negative cash flow.

Positive cash flow indicates that your business’s liquid assets are increasing since you have more cash entering than leaving.

How To Prepare a Cash Flow Statement

You know what a cash flow statement tells you. Let’s prepare and read one.

If you have a dedicated accountant for your business, that’s the person who typically prepares the cash flow statement.

If you use accounting software like Quickbooks for your bookkeeping, you can run a statement of cash flows in the reporting section of your software.

Otherwise, you can download a cash flow statement template to use in Microsoft Excel or other spreadsheet tools and prepare the statement manually.

You can create a cash flow statement for any period of time, but it’s usually done monthly or quarterly.

How To Read a Cash Flow Statement

Once you’ve generated a cash flow statement, it’s time to take a look at how you’re managing your money.

As mentioned before, your cash flow statement contains your opening balance, your closing balance, the net increase in cash, and your cash flows separated into three categories.

Let’s say you own a construction company called One World Construction, and you decide to run a cash flow statement for the third quarter of the year (July 1 through September 30).

In this example, One World Construction has an open balance of $9,847 at the start of the third quarter labeled “Cash at Beginning of Quarter.”

Here’s how to break down each section of the cash flow statement.

Cash From Operating Activities

First, you’ll see the “Cash from operating activities” section, which represents all sources and uses of cash related to business activities. Simply put, it includes cash used to create products and the cash generated by the sale of those products.

Operating activities can include:

- Revenue from the sale of goods and services

- Payments made to suppliers

- Payments for services used in production

- Payroll

- Interest payments

- Income tax payments

- Rent payments

- Administrative expenses

Each of the cash flow statement categories contains two sections: inflow and outflow. Cash outflows (cash leaving the business) are negative values and are represented by values in parentheses on the statement.

You’ll then see line items for each source and how much it cost. And, at the bottom, you can find the net cash flow.

Each section’s net cash flow is calculated by subtracting the cash leaving the business from the cash entering the business during the reporting period.

Let’s take a look at the example.

One World Construction brought in cash receipts from customers. And it used that cash to pay for inventory, administrative costs, payroll, interest, and income taxes.

During this reporting period, One World Construction had a net cash flow from operating activities valued at $36,128. This means that the business earned $36,128 more in revenue than it spent on operations.

Cash From Investing Activities

Cash from investing activities includes transactions related to assets, equipment, and investments fall in this category.

Some examples include advance loans made to vendors (for discounts) and the purchase or sale of equipment.

.png)

In our example, let’s say One World Construction sold some old equipment for $8,300 and purchased a new forklift for $42,300.

This would give them a negative net cash flow from investing activities of –$34,000. So, in this category, the business spent $34,000 more than it generated for the given period.

Cash From Financing Activities

Finally, we have cash flow from financing activities that outlines sources of cash from banks or investors and the cash you use to pay shareholders.

It shows money generated by issuing stock and money spent through buying back stock or paying shareholder dividends.

In our example, One World Construction is a privately held company, so we only see cash generated from borrowing and the cash used to pay down debt principal.

During this quarter, One World Construction obtained $15,000 as a new business loan and used $3,100 for repaying the principal amount on existing debt. This gives them a positive net cash flow from financing activities valued at $11,900.

Disclosure of Noncash Activities

Sometimes, you may need to provide details about noncash financing and transactions.

Both the International Finance Reporting Standards and the U.S. Generally Accepted Accounting Principles (U.S. GAAP) require you to include a disclosure of noncash activities along with your cash flow statement.

According to the above accounting standards, the disclosure of noncash activities is not included in the body of the cash flow statement. Instead, it’s attached as a footnote.

Examples of noncash activities you might need to disclose include issuing stock to pay down debt, purchasing assets with stock, conversion of debt to common stock, or conversion of preferred stock to common stock.

If you don’t issue stock, or you’re preparing a cash flow statement for internal review only, you can usually skip this step. Otherwise, if you’re submitting a cash flow statement to potential investors or lenders, they can tell you if they want disclosure of noncash activities.

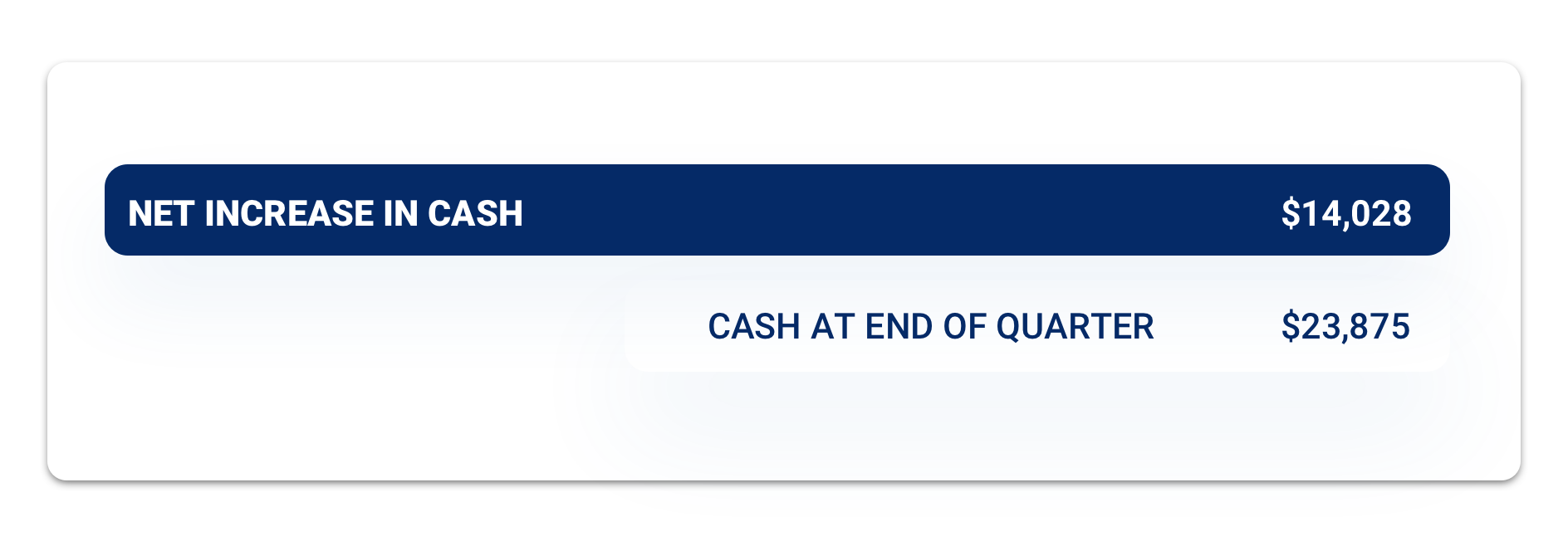

Net Increase in Cash

At the bottom of your cash flow statement, you’ll see the net increase in cash and closing balance of your business accounts at the end of the reporting period.

Your net increase in cash can be calculated by adding the net increase in cash for each of the three cash flow sections.

You should get the same value when you subtract your opening balance from your closing balance.

It tells you how much cash and cash equivalents you have at the end of the period and how that amount compares to your opening balance.

If your net increase in cash is positive, then your business has brought in more cash and cash equivalents than it has used during the reporting period. You have a positive cash flow.

If the net increase in cash is negative, this means you have an overall negative cash flow, and more cash has left your business than was brought in.

Keep in mind that the cash flow statement only records cash and cash equivalents, so your net increase in cash is not the same as net income or profit.

Two Methods for Calculating Cash Flow

You can choose from one of two methods when creating your cash flow statement: direct and indirect.

These two methods only affect the operating section. There are no differences when calculating cash flow for the investing and financing sections.

So, let’s take a look at these two methods.

Direct Cash Flow

As the name suggests, the direct method only records your business’s actual cash inflows and outflows. In other words, the money has to enter or leave your account during the reporting period to count.

The direct method for cash flow calculation can be appropriate for small businesses that use cash accounting instead of accrual accounting.

Cash basis accounting recognizes income only when it hits your bank account and expenses when they are paid, while accrual accounting recognizes revenue when its earned and expenses when they are incurred, regardless of when money changes hands.

Indirect Cash Flow

Instead of recording every actual cash transaction, the indirect method starts with your company’s net income (or net earnings) for the accounting period and converts accrual accounting to cash accounting.

Let’s say One World Construction received a purchase order valued at $3,000 on September 20, but they didn’t receive payment for the order until October 3.

Using the accrual basis for accounting, the $3,000 is recognized as revenue on September 20, which falls into the third-quarter reporting period (July 1 to September 30).

On the income statement, the purchase appears as a $3,000 increase in net earnings. It also appears on the September 30 balance sheet as $3,000 in accounts receivable. This means that your business has earned the revenue but did not collect it during the reporting period.

When preparing the cash flow statement using the indirect method, your accountant will use net earnings from the income statement as the basis for cash inflow.

But, since the cash hasn’t been collected for the $3,000 purchase, this amount needs to be offset somewhere else.

So, One World Construction would have a line item called “Increase to Accounts Receivable” valued at –$3,000 in the Cash from Operating Activities section.

Other standard adjustments used in the indirect method include:

- Recording payments made on previously placed orders

- Subtracting the cash used to purchase more inventory

- Subtracting cash used to pay vendors and suppliers

Comparing Cash Flow Methods: Which is Better?

Choosing the right cash flow method for you depends on your accounting method.

If you use cash-basis accounting, it will be easier to prepare a cash flow statement using the direct method. On the other hand, if you use accrual-basis accounting, then the indirect way of preparation is more manageable.

When comparing the two methods, the direct method provides the most accuracy, since you’re not making any adjustments. However, the direct method requires you to log every bank transaction, so it may take longer.

What Your Cash Flow Statement Can’t Tell You

The cash flow statement shows you how cash flows in and out of your business. It’s also an excellent way to see the different ways your business generates cash.

Like any financial statement, the cash flow statement can’t give you the entire picture of your business’s financial health.

Here are some of the insights you can’t get out of your company’s cash flow statement:

- Net income — As you can see from the direct and indirect method examples, the cash flow statement does not include income or losses from non-cash items, like depreciation or amortization (monthly debt payments), so it doesn’t show your entire net income.

- Profitability — Profit is calculated as net sales minus the cost of goods sold, and since the cash flow statement doesn’t include total sales or cost of goods sold it can’t be used to calculate profit.

- Future income potential — Cash flow statements are based on historical data. They can be used to watch for trends in your cash management, but they can’t predict future cash flow with total accuracy. The best way to project a company’s future income potential is by looking at past earnings. But even past earnings are subject to economic shifts and changes in supply and demand.

You need to consider your cash flow statement along with other financial reports and ratios (like cash ratio and quick ratio) when performing a complete financial analysis.

Cash Flow and Other Financial Statements

To get a comprehensive picture of your business’s financial health, it’s a good idea to look at it from several angles. While a cash flow statement shows you the cash you have on-hand and how cash has been generated and used, a balance sheet shows you a bigger picture of your financial position.

A balance sheet includes things like longer term liabilities (things you owe in the future) as well as non-cash assets, like inventory.

An income statement (also called a P&L or Profit and Loss Statement) shows you income or loss generated, and can include things like depreciation, which don't impact your cash balance—but you are essentially losing money on an item as its value declines over time.

Using these with a cash flow statement will help you check you have funds available when you need them. For example, if you have a large amount of income you notice on your income statement, but you don’t see the cash on your cash flow statement, then you might need to think of better ways to collect money for your services or products sold. Or maybe you need to rethink an equipment purchase or any other expenses you thought you could incur because your other financial statements were showing strong values.

And yet another example: Let’s say you're showing a lot of cash on your cash flow statement, but you have some long-term liabilities on the horizon, like deferred tax payments—which you can see on your balance sheet—you may want to rethink spending your cash.

Gain Insight from your Cash Flow Statement

A cash flow statement can give you important insights into your business activities and financial performance over a given period. It can help you decide if you need to create more ways to generate cash and if you have the ability to pay your bills. It’s also a tool used by banks and investors to gauge the health of your business. Use a cash flow statement, along with an income statement and balance sheet, to better understand the financial health of your business.

Ready to transform your business into a profit-pumping machine? Learn how with our monthly newsletter.